Interactive Textbook Market: Global Outlook, Trends, and Forecast to 2030

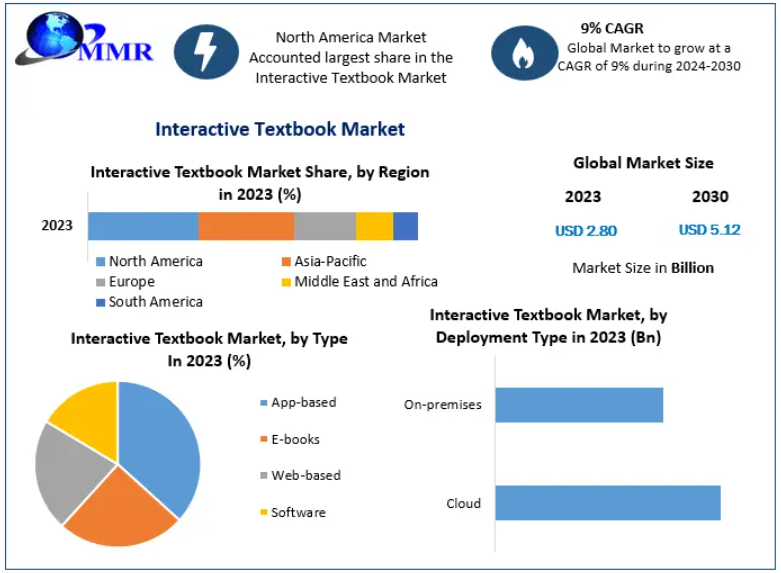

The Interactive Textbook Market is undergoing rapid digital transformation as educational institutions worldwide transition from traditional learning models to technology-driven ecosystems. Valued at USD 2.80 billion in 2023, the market is projected to reach USD 5.12 billion by 2030, expanding at a CAGR of 9% between 2024 and 2030. Interactive textbooks—enhanced with multimedia elements, analytics, gamification, and cloud capabilities—are redefining how students learn, collaborate, and engage with academic content.

Market Overview

Interactive textbooks, also known as digital or enhanced e-textbooks, represent the next generation of educational content delivery. Unlike simple e-books, these resources integrate:

- 3D models

- Short educational videos

- Interactive maps and infographics

- Quizzes and self-assessments

- Embedded audio narratives

Their multi-format approach caters to diverse learning styles, improves retention, and offers real-time feedback to students and instructors. Advancements in cloud technology, smart devices, and high-speed internet have accelerated adoption across schools and universities.

Instructors increasingly prefer interactive digital materials because they are easy to update, customizable to curriculum needs, and track student performance efficiently. Open-source interactive textbooks also provide flexible alternatives, enabling educators to develop personalized content at minimal cost.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/88932/

Market Dynamics

- Rising Adoption of Smart Education

The global shift toward smart education is one of the primary drivers of market growth. Students today expect dynamic, visually rich content that goes beyond text-heavy materials. Interactive textbooks foster engagement through:

- Gamified elements

- Problem-solving interfaces

- Instant scoring and feedback

- Multimedia-based explanations

This heightened engagement strengthens the student-teacher connection and significantly improves learning outcomes, making interactive textbooks a preferred digital tool.

- Growth in Digital Devices & Connectivity

The widespread availability of smartphones, tablets, and low-cost laptops has expanded digital education access. Modern digital devices offer powerful processing capabilities that support advanced features such as Augmented Reality (AR), enabling truly immersive learning experiences.

Additionally, rapid global internet penetration—especially in emerging economies—supports cloud-based deployments, allowing students to access content anytime, anywhere.

- Expansion of Cloud-Based Interactive Textbooks

Cloud deployment is expected to grow at a robust 9.4% CAGR through 2030, making it the fastest-growing segment. Cloud-based platforms offer advantages such as:

- Easy integration and implementation

- Real-time updates

- Multi-device synchronization

- Lower storage requirements

- Scalability for institutions

Publishers leveraging cloud frameworks can incorporate AR/VR, analytics, and collaborative tools seamlessly, boosting market expansion.

- Cost Barriers Restricting Adoption

Despite numerous advantages, the high cost of interactive textbooks and supporting devices remains a major restraint, particularly in underfunded educational systems. Licensing fees, proprietary formats, and premium digital infrastructure also pose challenges to broader adoption.

Segmentation Analysis

By Type

- App-based

- E-books

- Web-based

- Software

Web-based and app-based formats dominate due to ease of use and compatibility with mobile devices and learning management systems (LMS).

By Deployment Type

- Cloud (fastest growing)

- On-premises

Cloud dominates due to reduced overhead costs and improved accessibility.

By Application

- K–12 Schools

- Higher Education Institutions

- Others (corporate training, professional certification)

K–12 remains a major revenue generator, while higher education institutions adopt interactive textbooks to enhance hybrid and online learning environments.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/88932/

Regional Insights

North America Leads the Market

Holding 57.9% market share in 2023, North America remains the global leader due to:

- Widespread adoption of smart classrooms

- Mature cloud infrastructure

- High student engagement with digital learning tools

- Strong presence of interactive textbook developers

- Rising preference for analytics-enabled educational content

The U.S. features several free and low-cost providers—including MathScribe—that further support market scalability. The competitive landscape is vibrant, with established publishers and disruptive ed-tech start-ups offering innovative solutions.

Europe

Strong growth driven by government-backed digital education reforms and demand for multilingual interactive content.

Asia-Pacific

Expected to witness the fastest growth, especially in China, India, Japan, and South Korea, where EdTech investments are skyrocketing.

Middle East & Africa / South America

Growth is accelerating as institutions embrace remote learning, digital literacy programs, and affordable smart devices.

Competitive Landscape

The market features a blend of global publishing houses, technology companies, and EdTech innovators. Key players focus on enhancing content quality, personalizing learning experiences, and integrating AI, AR, and analytics.

Key Companies

- Apple

- Cambridge University Press

- Houghton Mifflin Harcourt

- John Wiley & Sons

- McGraw-Hill Education

- Oxford University Press

- Pearson Education

- VitalSource

- Metrodigi

- Kortext

- Others (emerging EdTech developers)

These organizations are investing heavily in cloud delivery, mobile-first content design, interactive platforms, and customizable digital learning ecosystems.

Conclusion

The Interactive Textbook Market is poised for strong expansion as digital learning becomes central to global education systems. With increasing demand for immersive, data-driven, and flexible content, publishers and EdTech companies are rapidly innovating to meet evolving classroom needs.

Cloud adoption, multimedia integration, and accessibility via smart devices will remain key growth drivers through 2030. Although cost barriers persist, the shift toward digital-first education presents major opportunities for both new entrants and established market leaders.